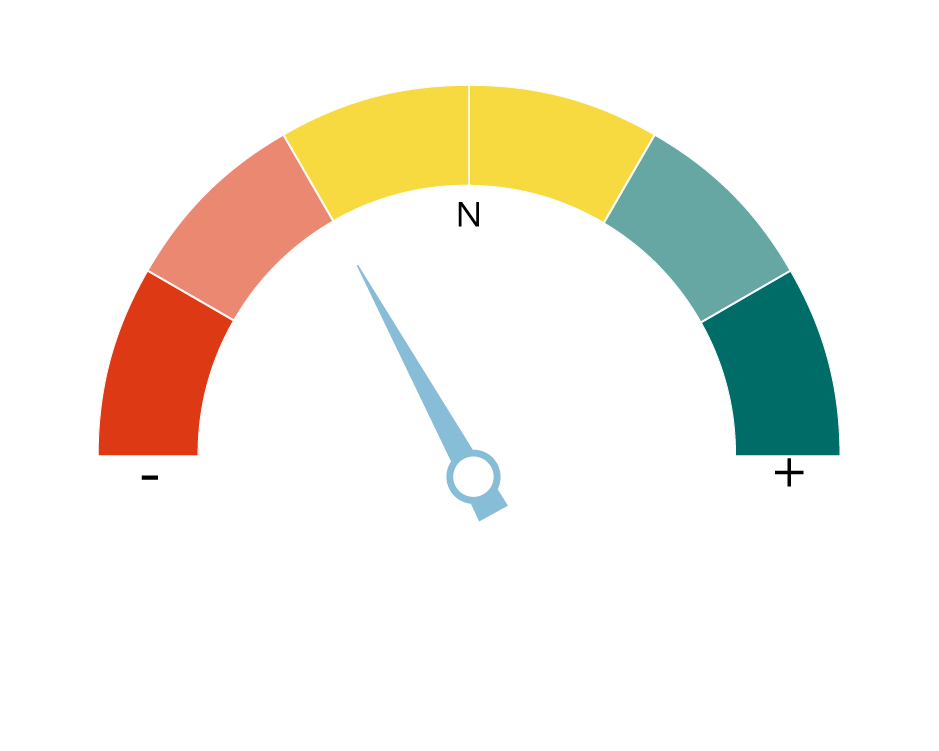

Our increased US investment grade (hedged) bond exposure has been funded by a reduction in our exposure to European and UK investment grade bonds. This slightly increases our sensitivity to interest rate changes, as we have stronger conviction that Fed rates have peaked and we’re positioning for falling bond yields in the US.

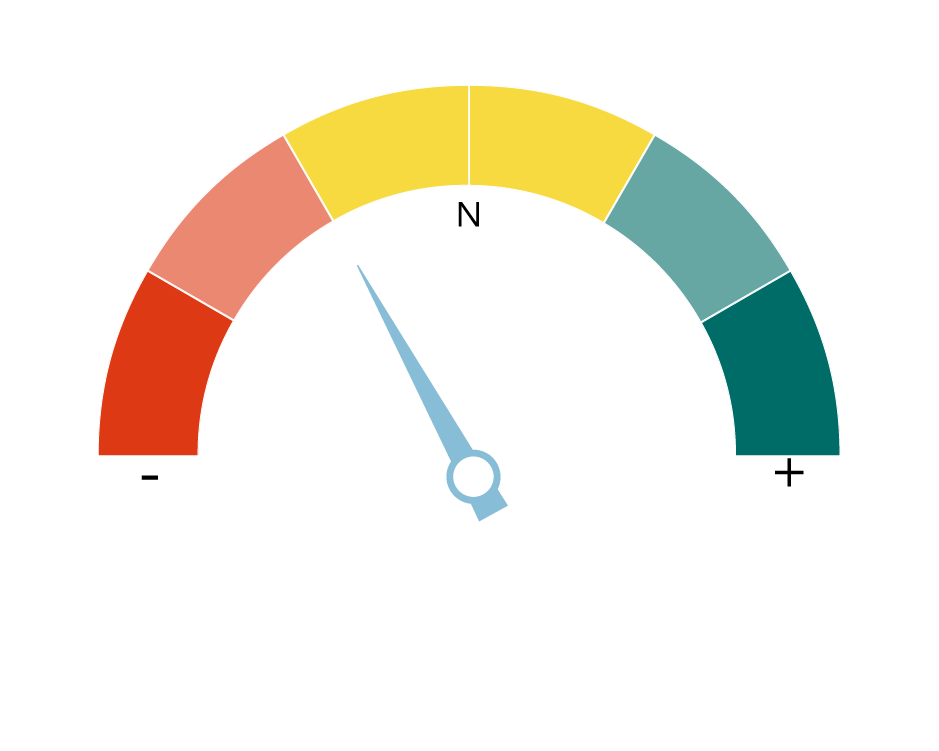

Our analysis suggests that the outlook for continued outperformance of Eurozone equities is likely to become more challenged. However, there are risks in the US market given stretched valuations and our belief that expectations of Fed rate cuts are too optimistic. We see European minimum volatility stocks as a way of increasing our exposure to the Eurozone and allowing us to diversify away from the US, while keeping our slightly reduced exposure to equities unchanged. By investing broadly into Europe (rather than just Eurozone equities), we are positioned capture any continued upside in Eurozone equities while mitigating the risks of a downturn through wider regional diversification and a focus on defensive sectors and companies.

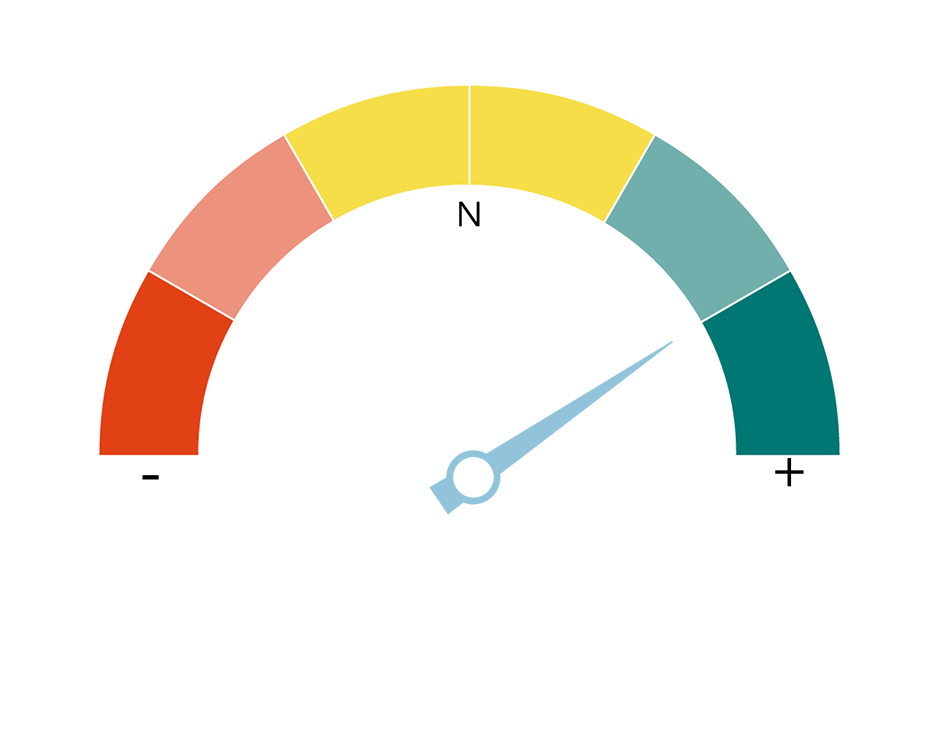

Our overall equity exposure is still marginally reduced vs our strategic (long-term) asset allocation. Although stock markets have performed relatively well this year, we do not think it is yet the time to increase exposure to risk in our portfolios.

We maintain a slightly cautious stance on credit, mainly the US high yield market, where banking-sector stresses, tighter credit standards and rate rises will likely be most acutely felt.

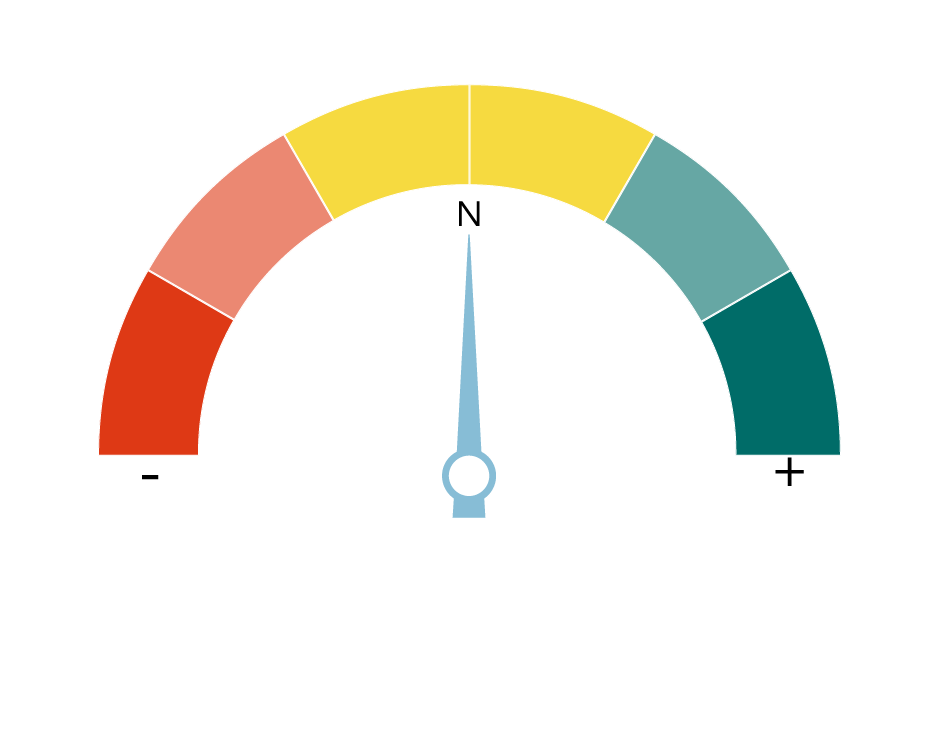

We maintain our local cash balances and hold gold as a strategic hedge at a neutral level relative to our new long-term allocation. We add exposure to a new asset class: hedge funds.

Information correct as at 25 May 2023

This document is designed as marketing material. This document has been composed by Brown Shipley & Co Ltd ("Brown Shipley”). Brown Shipley is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. Registered in England and Wales No. 398426. Registered Office: 2 Moorgate, London, EC2R 6AG.

This document is for information purposes only, does not constitute individual (investment or tax) advice and investment decisions must not be based merely on this document. Whenever this document mentions a product, service or advice, it should be considered only as an indication or summary and cannot be seen as complete or fully accurate. All (investment or tax) decisions based on this information are for your own expense and for your own risk. You should (have) assess(ed) whether the product or service is suitable for your situation. Brown Shipley and its employees cannot be held liable for any loss or damage arising out of the use of (any part of) this document.

The contents of this document are based on publicly available information and/or sources which we deem trustworthy. Although reasonable care has been employed to publish data and information as truthfully and correctly as possible, we cannot accept any liability for the contents of this document, as far as it is based on those sources.

Investing involves risks and the value of investments may go up or down. Past performance is no indication of future performance. Currency fluctuations may influence your returns.

The information included is subject to change and Brown Shipley has no obligation after the date of publication of the text to update or amend the information accordingly. Accordingly, this material may have already been updated, modified, amended and/or supplemented by the time you receive or access it.

This is a non-independent research and it has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and that it is not subject to any prohibition on dealing ahead of the dissemination of investment research.

All copyrights and trademarks regarding this document are held by Brown Shipley, unless expressly stated otherwise. You are not allowed to copy, duplicate in any form or redistribute or use in any way the contents of this document, completely or partially, without the prior explicit and written approval of Brown Shipley. Notwithstanding anything herein to the contrary, and except as required to enable compliance with applicable securities law. See the privacy notice on our website for how your personal data is used (https://brownshipley.com/en-gb/privacy-and-cookie-policy).

.png?width=650&resizemode=force)