.png)

Daniele Antonucci

Co-Head of Investment & Chief Investment Officer

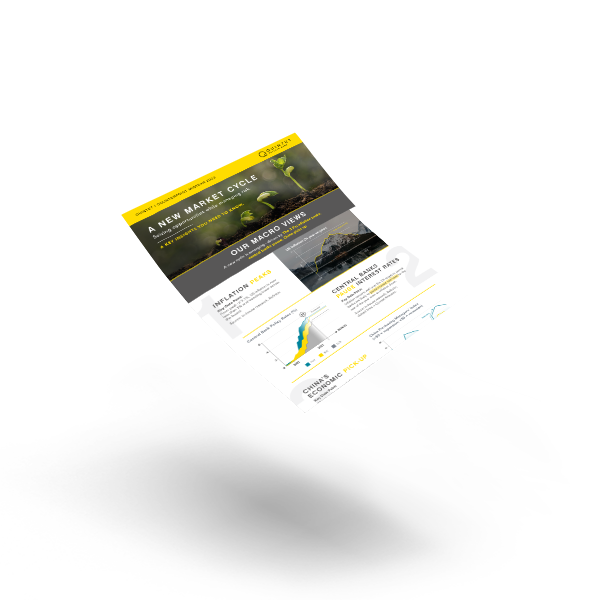

As we reach the midpoint of 2023, it's worth revisiting the predictions we made earlier in the year. Specifically, our three key macro calls that would take place around Q2: a peak in inflation (starting with the US), a pivot in central bank interest rate policy (starting with the US Federal Reserve, Fed), and a pick-up in China's growth. We refer to these as “the three Ps”.

The macro rationale behind these calls was based on the expectation of a recession in developed markets due to monetary tightening, which would curb inflation and lead central banks to pause rate increases. Meanwhile, a recovery would gain momentum in China, where there is no inflation problem but, rather, central bank stimulus and reopening.

So, were our predictions right? Yes, partly. Inflation is showing clear signs of moving past the peak (in the US at least), leaving the door open for the Fed to pause its interest rate hiking cycle, and China’s growth has accelerated sooner - though perhaps less strongly - than expected and recent indicators point to slower progress. However, the prediction of a developed market recession has not yet come to fruition. Developed markets have proven to be more resilient than expected – the Eurozone and the UK in particular – thanks largely to energy disinflation and a mild winter, despite periods of weak growth. However, given the lagged impact of past interest rate hikes and the credit squeeze we envisage, a mild recession in the US now looks more likely in the second half of this year.

So, has our outlook changed as we look ahead to the rest of the year and beyond? Not a huge amount. We continue to believe we will see a divergence of growth and the emergence of new market cycles, driven by the so-called “three Ps”. We think the Eurozone and UK are probably where the US was six months ago, with inflation yet to peak convincingly and central banks looking to continue to raise rates – although not for long. Therefore, the balance of risks is skewed towards more European Central Bank and Bank of England hikes vs Fed.

We also think the currency outlook is unlikely to shift significantly over the next couple of quarters. We believe the US dollar (USD) remains overvalued and the Fed pausing rates could lead to some USD weakness. As the Fed pauses, the real interest rate differential between the US and the Eurozone/UK should diminish. The euro and pound sterling should strengthen vs the USD, though moderately given weak domestic growth.

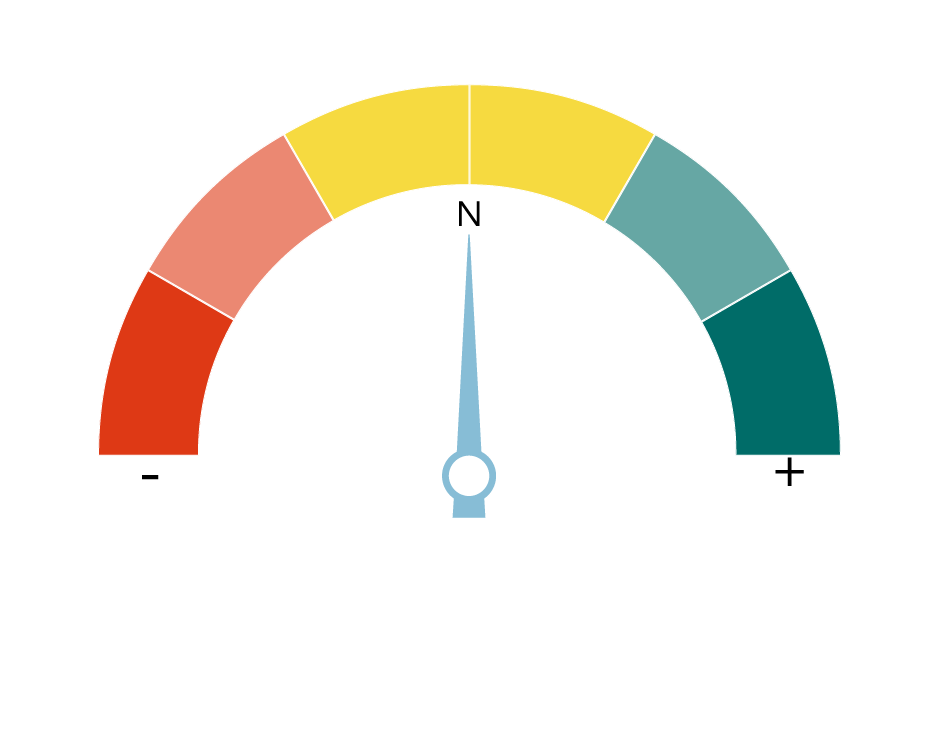

When it comes to the market landscape, our overall stance is also largely unchanged. Relative to our long-term asset allocation, we are allocating slightly more to high-quality bonds and slightly less to equities and credit, given market uncertainty and that we think the peak in interest rates is in sight. So, rather than an overhaul of our asset allocation, we’ll continue to make tweaks as trends and risks emerge.

Importantly, we have introduced a key long-term diversifier in our UK flagship portfolios - hedge funds - funded predominantly via reducing our gold allocation. Gold as an asset class provides attractive hedging properties by historically performing well in crisis periods. We decided to add hedge funds alongside gold as our historical analysis shows this would have led to improved risk-adjusted returns, lower volatility and less severe drawdowns. The goal is to achieve greater diversification. In this vein, we allocate to a blend of managers pursuing different investment strategies to reduce manager-specific risk.

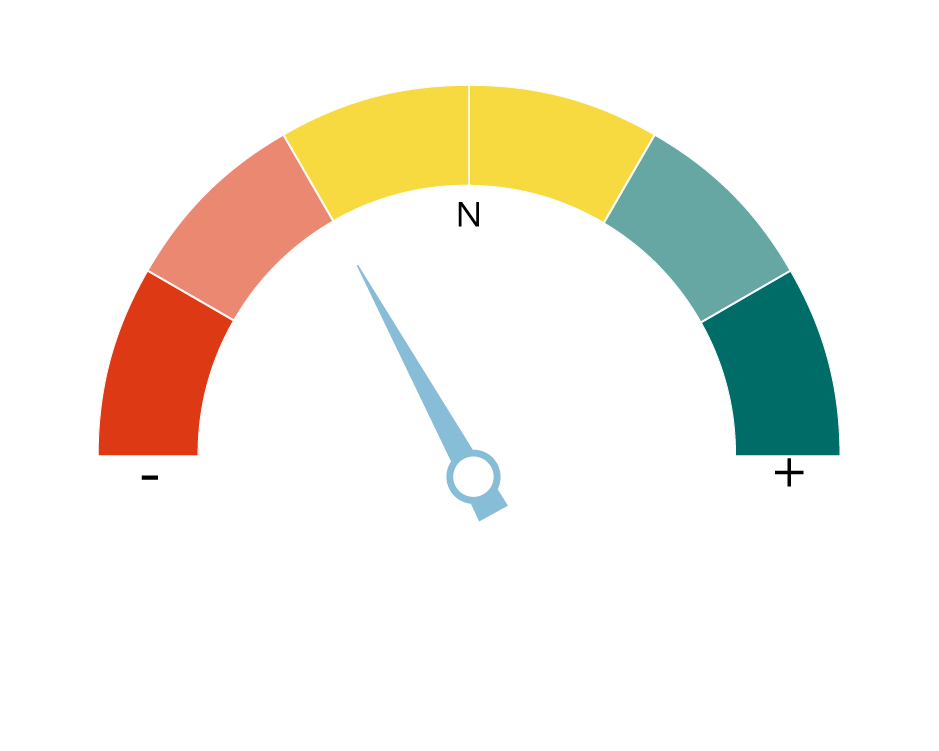

Our overall equity exposure is still marginally reduced vs our strategic (long-term) asset allocation. Although stock markets have performed relatively well this year, we do not think it is yet the time to increase exposure to risk in our portfolios.

Read more

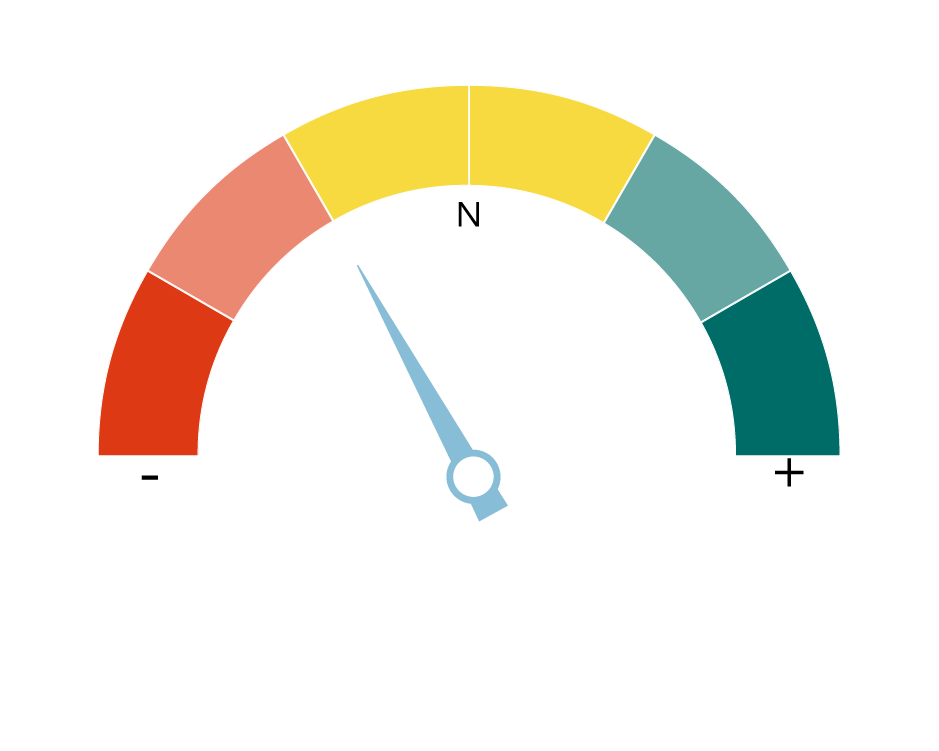

We maintain a slightly cautious stance on credit, mainly the US high yield market, where banking-sector stresses, tighter credit standards and rate rises will likely be most acutely felt.

Read more

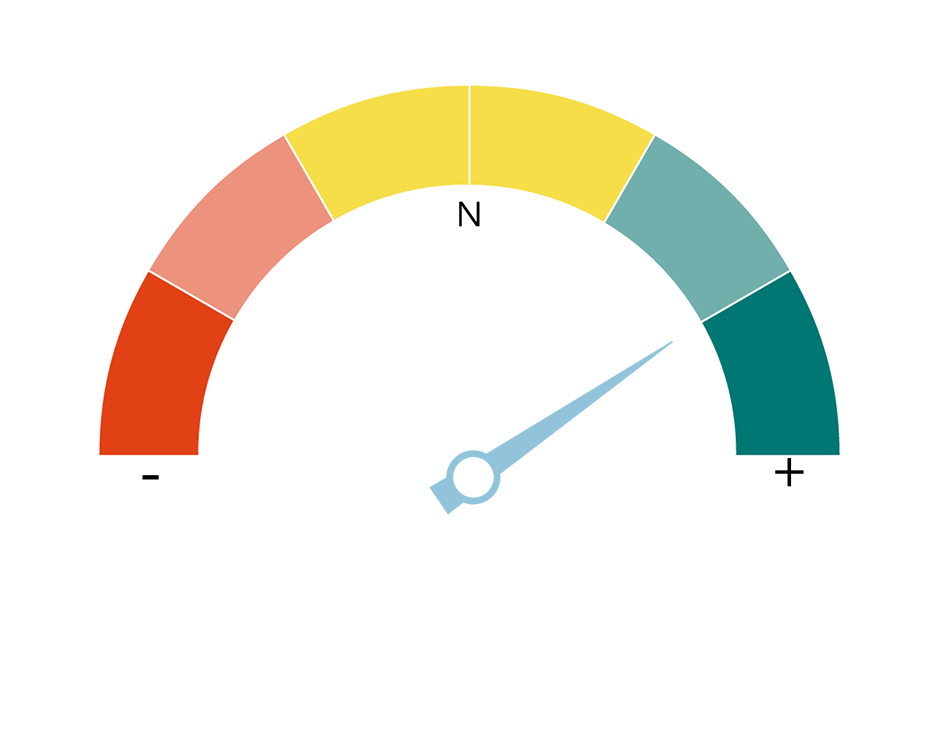

We maintain our local cash balances and hold gold as a strategic hedge at a neutral level relative to our new long-term allocation. We add exposure to a new asset class: hedge funds.

Read more

Information correct as at 25 May 2023

This document is designed as marketing material. This document has been composed by Brown Shipley & Co Ltd ("Brown Shipley”). Brown Shipley is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. Registered in England and Wales No. 398426. Registered Office: 2 Moorgate, London, EC2R 6AG.

This document is for information purposes only, does not constitute individual (investment or tax) advice and investment decisions must not be based merely on this document. Whenever this document mentions a product, service or advice, it should be considered only as an indication or summary and cannot be seen as complete or fully accurate. All (investment or tax) decisions based on this information are for your own expense and for your own risk. You should (have) assess(ed) whether the product or service is suitable for your situation. Brown Shipley and its employees cannot be held liable for any loss or damage arising out of the use of (any part of) this document.

The contents of this document are based on publicly available information and/or sources which we deem trustworthy. Although reasonable care has been employed to publish data and information as truthfully and correctly as possible, we cannot accept any liability for the contents of this document, as far as it is based on those sources.

Investing involves risks and the value of investments may go up or down. Past performance is no indication of future performance. Currency fluctuations may influence your returns.

The information included is subject to change and Brown Shipley has no obligation after the date of publication of the text to update or amend the information accordingly. Accordingly, this material may have already been updated, modified, amended and/or supplemented by the time you receive or access it.

This is a non-independent research and it has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and that it is not subject to any prohibition on dealing ahead of the dissemination of investment research.

All copyrights and trademarks regarding this document are held by Brown Shipley, unless expressly stated otherwise. You are not allowed to copy, duplicate in any form or redistribute or use in any way the contents of this document, completely or partially, without the prior explicit and written approval of Brown Shipley. Notwithstanding anything herein to the contrary, and except as required to enable compliance with applicable securities law. See the privacy notice on our website for how your personal data is used (https://brownshipley.com/en-gb/privacy-and-cookie-policy).

.png?width=650&resizemode=force)