How to Use Charitable Giving as Part of Your Philanthropy Strategy

Many people find it rewarding to support a charity or cause they care about. Whether you give in your lifetime, leave a legacy or do both, it’s a pleasure to know that you’ve made a difference.

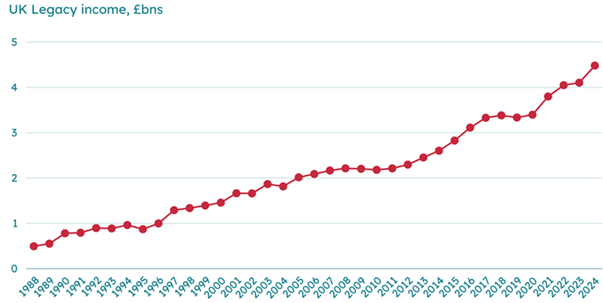

If you’re leaving a legacy, you’re in great company. There’s a mini-boom in doing so, as UK legacy income reached a record £4.5bn in 20241, up 9% on the year before.

That’s a welcome lifeline for many charities, as the number of regular donations is falling amid a cost-of-living crisis and lack of interest. The proportion of people donating to charities fell to 50% in 20242, the lowest level since the Charities Aid Foundation started tracking the metric in 2016.

Supporting good causes is important to many people. Some choose to divide their wealth between family and charitable interests, while others prefer to focus more fully on philanthropy or foundations. Whatever your plans, we can help you structure your charitable giving in a way that aligns with your goals and ensures your support is directed where you intend it to be. While mitigating the inheritance tax (IHT) payable at the same time.

UK legacy income reaches £4.5bn in 2024

Source: The Legacy Giving Report 2025. Smee & Ford.1

The importance of Philanthropy in Wealth Management

Across the globe, philanthropy plays an important role in wealth management. High-net-worth individuals (HNWIs) have a record of giving back to the societies that nurtured them. Notably, the Victorian industrialists built social housing, and today under the US Giving Pledge wealthy individuals give away half their fortunes.

If you feel that philanthropy is important, it can form an integral part of your wealth management strategy. What’s more, the government incentivises family wealth philanthropy by offering tax breaks in your lifetime and if you leave a legacy on your death.

To better understand how you can incorporate philanthropy into your wealth management plan, download our comprehensive 'Essential Guide to Passing On Wealth.' This guide provides valuable insights on making your charitable giving both impactful and tax-efficient.

Why Philanthropy matters for HNWIs

There’s a strong tradition of philanthropy among many HNWIs. A number of these individuals are entrepreneurs, bringing experience of shaping change through having a clear vision and pursuing it to fruition. Modern forms of philanthropy and charitable giving are similar, with their emphasis on measurable outcomes rather than simply giving.

For example, you could make a gift to a school or college specifically with the goal of increasing literacy rates among children aged 6–8 in a target region from 65% to 80% within three years.

The role of charitable giving in shaping a legacy

For some, part of the appeal of leaving of philanthropy can include leaving a legacy. You may want to achieve something beyond your working life that’s good for your society, or even the community where you live.

In days gone by, people granting legacies often left their names on buildings or museums, whereas today, Family Wealth Planning may play a role in shaping outcomes or reflecting your values, though approaches can differ. You might, for example, back a charity dedicated to reducing knife crime or make a gift to your old school targeted at improving facilities for a certain subject.

Charitable giving strategies for purpose-driven Wealth Management

Depending on what you want to achieve, and how much you want to give, there’s a range of ways to go about charitable giving. We can guide you on approaches that will help you pursue your wealth and philanthropy goals and support the impact you wish to achieve.

Direct giving: The simplest way to make an impact

Giving directly during your lifetime can be a straightforward way to support the causes that matter to you. It allows you to provide help to a charity, school, or community foundation without taking on ongoing administrative commitments.

If you choose to give money during your lifetime, the charity you support may be able to claim Gift Aid, depending on its eligibility. This government scheme allows charities to increase the value of a donation by reclaiming tax paid on it by the donor.

Giving non-cash assets: An evolving practice

You might want to give away illiquid assets like shares, property or art. This can be a tax efficient way to give.

For many clients, philanthropy is a vital part of their wealth management strategy. You may want to split your wealth between family and good causes. If so, we can advise you on how you can you pursue your philanthropic goals within the scope of your broader wealth management objectives.

Depending on what you want to achieve, you can choose from a range of different giving structures. Each has particular characteristics that may make it suitable.

Charitable Trusts: Structuring long-term giving

If you want to organise your charitable giving over time, setting up a Trust can be be a straightforward approach for many people. A trust is a legal structure that allows you to set aside funds for a specific purpose that will be managed by your nominated trustees.

The trust deed specifies the charitable purposes such as education, community or health. Additionally, you can involve your children by appointing them as trustees.

Donor-Advised Funds (DAFs): Combining flexibility and vision

If you want an alternative, you can set up a DAF. A DAF is an individual charitable fund set up under a sponsoring charity. This acts as an umbrella, holding DAFs on behalf of multiple clients underneath – you can think of it as a charitable giving account from which you can make donations. You can put money or other assets in a DAF and support charities in the UK or worldwide. The DAF takes care of all administration and reporting, charging a fee. You can even appoint an investment manager to look after your money in the DAF.

Private foundations: For significant legacies

If you want to have a truly bespoke arrangement, you might consider setting up a foundation. This approach is often chosen by individuals who wish to take an active role in philanthropy and make very large gifts. If you want to have a truly bespoke arrangement, you might consider setting up a foundation. This approach is often chosen by individuals who wish to take an active role in philanthropy and make significant gifts. You can choose how much or little involvement you have. You can be the public face and it can carry your name – or you can be anonymous. Perhaps you want to involve your children and grandchildren, so you know the good work will live on? Setting up a foundation requires professional advice and carries ongoing administration and reporting responsibilities.

Whatever route you choose, philanthropy can be a meaningful way to support the causes that matter to you. Whether giving in your lifetime or leaving a legacy, your contribution can help change lives in many different ways.

Get in touch with a Brown Shipley Client Advisor to learn more about philanthropy wealth management.

1 Smee & Ford – Legacy Giving Report 2025 https://smeeandford.com/reports-whitepapers/legacy-giving-report-2025/

2 Charities Aid Foundation – UK Giving Report 2025 https://www.cafonline.org/docs/default-source/uk-giving-reports/uk_giving_report_2025.pdf

Important Information

Information correct as of 24 April 2026.

- Investing puts your capital at risk.

- This is a Marketing communication.

- Brown Shipley is authorised and regulated by the Financial Conduct Authority and the Prudential Regulation Authority.

- The value your investments or any income from them can go down as well as up, and you could lose some or all of the money.

- Tax treatment depends on individual circumstances and is subject to change.

- We recommend that you seek professional legal and tax advice to understand your personal tax liabilities. This will depend on personal circumstances and the prevailing tax rules, which are subject to change.

- Tax planning is not regulated by the Financial Conduct Authority or the Prudential Regulation Authority.

- This article/blog is for informational purposes only and does not constitute financial or legal or tax advice.

This document is for information purposes only, does not constitute individual (investment or tax) advice and investment decisions must not be based merely on this document. Whenever this document mentions a product, service or advice, it should be considered only as an indication or summary and cannot be seen as complete or fully accurate. All (investment or tax) decisions based on this information are for your own expense and for your own risk. You should (have) assess(ed) whether the product or service is suitable for your situation. Brown Shipley and its employees cannot be held liable for any loss or damage arising out of the use of (any part of) this document.